Living in Florida comes with its own rhythm. Sunshine stretches across balconies, palm trees gossip with the breeze, and every so often, the weather reminds residents why insurance matters. For those living in condominium associations (COAs) and homeowners associations (HOAs), understanding the difference between condo insurance and homeowners insurance is more than paperwork—it is financial protection woven into community life.

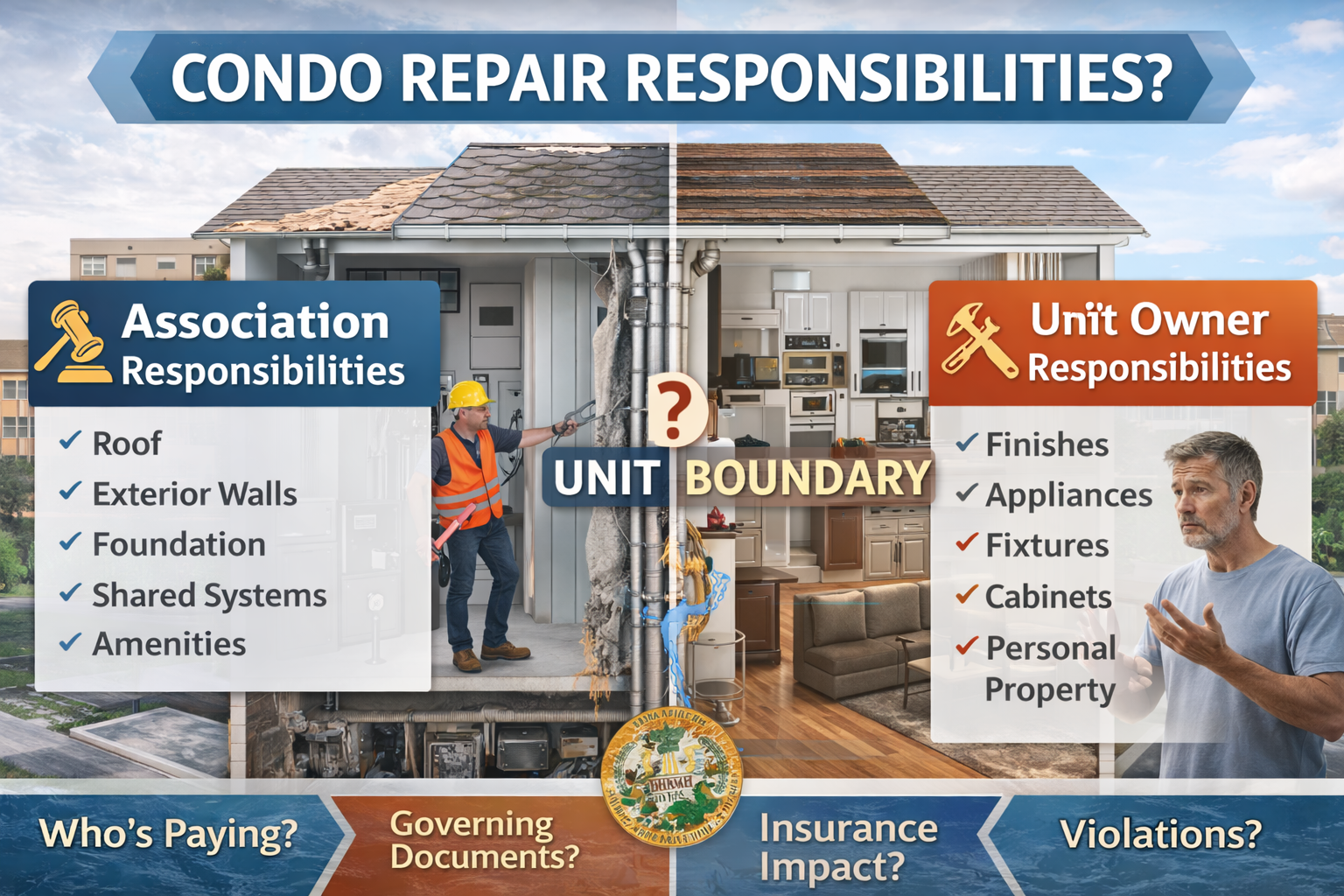

In a condominium association, the building itself is a shared responsibility. The association typically carries a master insurance policy covering the structure, roof, exterior walls, and common areas. Florida law requires COAs to maintain specific property and hazard coverage, which means an individual condo policy—commonly known as an HO-6 policy—focuses primarily on the interior of the unit and personal belongings.

Interior coverage usually includes flooring, cabinetry, built-ins, fixtures, and contents. However, coverage boundaries are not identical across associations. Some COAs follow a “bare walls” approach, where everything from the drywall inward belongs to the owner. Others provide more extensive “all-in” coverage that includes certain interior finishes. Reviewing both the association’s declaration and master policy is essential, especially in Florida, where hurricane deductibles and claim responsibilities can create gray areas.

Loss assessment coverage is particularly important for condo owners. If a major storm or incident damages common elements and the association’s insurance falls short, owners may be assessed their share of the difference. Many HO-6 policies offer optional loss assessment coverage, helping turn what could be a financial tidal wave into a manageable ripple.

Homeowners living within HOAs operate in a different insurance framework. While the association may insure shared amenities such as clubhouses, entry features, pools, or landscaping, the home itself is fully the owner’s responsibility. A standard homeowners policy (HO-3) covers the dwelling, interior, detached structures, personal property, liability, and additional living expenses if the home becomes uninhabitable.

Florida homeowners often face added considerations, including windstorm deductibles, roof coverage limitations, and carrier availability. Flood insurance is also worth careful consideration, as standard policies typically exclude flood damage—even outside designated flood zones.

For both COA and HOA residents, liability protection is just as critical as property coverage. The association’s policy protects common areas, while personal policies protect individual households. Together, they form a shared safety net. A brief conversation with both your insurance agent and your association can help close coverage gaps before the next storm or surprise repair arrives.